We are currently living through an extremely interesting time for our nation. While things are always in a constant state of flux and changing all around us, it seems like the pace of change has picked up lately and spread to nearly every part of our lives.

Civilians may have a far easier time adjusting to these changes than military members and families because they have options. Whether it be the desire to search for a new job, move to a new location of their choosing, or change many of their life circumstances, they have options that military members and families do not. While the general public is not contractually tied down by things like where they live or work, in the military we have a mission and a duty to our nation, and we will fulfill it to our greatest ability.

One of the largest monthly expenses for most Americans is either their rent or mortgage, and the largest purchase that most Americans ever make is for their home. These large expenditures also entail some unique challenges for military members and their families, which may change the calculus on whether you decide to buy, rent, sell, or rent out your home.

In this article, we will cover what drives the costs of real estate, what is currently seen in the U.S. economy and housing market, and offer perspectives for you to consider when deciding what the near future holds for you in terms of housing.

Image from Canva

Image from Canva

The Economics of Home and Rental Prices

When most people think of real estate, they only consider whether we are in a “buyer’s market” or a “seller's market.” A large component of which type of real estate market we are in at any given time has to do with whether there are more sellers or buyers, but that is far from the only component that drives whether it is a good time to buy or sell.

Supply and Demand

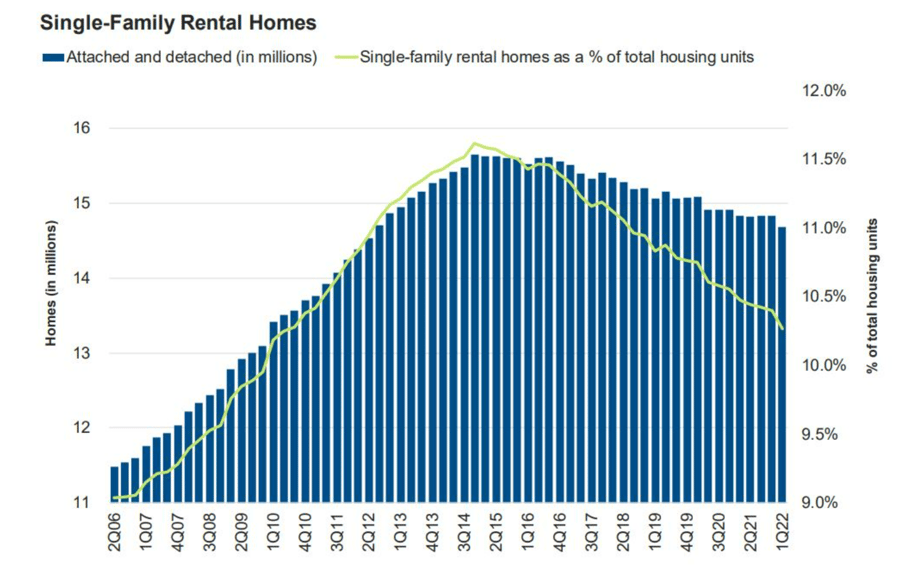

As with most goods, a large aspect of real estate prices is supply and demand. These metrics can be decidedly more critical with real estate, however, as it takes far longer to build a new home or apartment building than it does to produce more Coca-Cola or electronic gadgets.

When asked by Forbes Advisor about the rapid rise of home prices over the past few years, EVP of RealtyTrac Rick Sharga responded,

“The supply-demand imbalance is the primary reason home prices have escalated so rapidly. And after not building nearly enough houses for the last decade, homebuilders will take several years at least to add enough new supply to balance the market.”

Sharga went on to explain just how out of balance the supply and demand curve is in our current market:

“In a balanced market, the months of supply would be around six months– the time it would take to deplete all homes for sale at the current sales pace. But today’s market has only 1.7 months of supply, showing a drastic imbalance in favor of sellers.”

Political and Regulation Risk

One of the greatest reasons for the supply and demand imbalance, especially in highly populated areas like San Francisco and Los Angeles, are regulations or the fear by homebuilders of new regulations regarding building. In highly regulated markets like those listed above, it can take years for commercial real estate builders to get the necessary approvals to build a new apartment or condominium complex or even new houses.

Commercial real estate builders may be willing to take that risk for long-term projects when the economy is doing well, but when times get tight they are far less willing. With our current political climate and process of changing government leadership every two to six years, there's a significant risk to these builders that a new city, state, or even federal administration will take office and make changes that could cost them greatly.

A Nashville-based home builder was quoted in the June report released by John Burns Real Estate Consulting as saying, “Scary times. Hoard cash and hang on for the ride!” If both commercial and residential builders are wary of making significant investments in building new properties at the moment, the supply side of the equation may become greatly impacted.

To take an example from a metropolitan area well known for extremely high rent prices, San Francisco went on a nine-year increase in housing supply in the last decade but has been on a significant supply decrease for the past seven years. These regulatory increases that led to lowered supply happened as Silicon Valley was growing by leaps and bounds, leaving rents there virtually unaffordable for most:

Source: John Burns Real Estate Consulting

Source: John Burns Real Estate Consulting

Mortgage Rates

On the opposite side of the equation, the financials play an extremely important role in real estate beyond the supply and demand equation. Even if supply and demand are perfectly even, rising mortgage rates or lowering credit scores have an outsized role in whether or not people can afford to even buy a home, thereby affecting the demand.

According to the latest US Census, roughly 70% of Americans take on mortgages to buy their homes. This means that mortgage rates, which are directly influenced by interest rates, play a large role in who can afford to purchase a home.

.png?width=700&name=2022-08-04%20(1).png) Source: https://buckrail.com/new-year-new-home-interest-rates-can-help/

Source: https://buckrail.com/new-year-new-home-interest-rates-can-help/

Our nation has lived under abnormally low interest rates since the 2008-09 housing crisis, the federal reaction to which created an extremely low interest rate environment. This means that savers received virtually no interest on their savings accounts or Certificates of Deposit (CDs) in banks, but also meant that those who could be approved to take out new loans were given very low rates.

With inflation now topping the highest rates that we’ve seen since the 1970s, The Federal Reserve is rapidly increasing the Federal Funds Rate (the benchmark interest rate that drives other rates in our nation). The Federal Reserve meets every month in their Federal Open Market Committee (FOMC) meetings, at which they determine what the rates should be in order to keep inflation within their defined targets.

As the indicators that they follow are all lagging, it's forecasted by both economists and analysts at the largest banks that these rates will continue to be raised for the foreseeable future. And every time The Federal Reserve increases its rates, mortgage rates will typically rise along with them.

The graphic above gives a prime example of just how important this is to potential home buyers. The tables show how expensive of a home a borrower with $2,000 or $5,000 available monthly to spend on mortgage payments can afford to buy. While the interest rates in these tables only vary by two percentage points, you can see the wide disparity these small changes can make in what the borrower can afford.

The real estate platform Redfin reported in its latest report that 60,000 home purchases fell through in June of 2022, which is the highest rate since 2020. Many real estate professionals are speculating that this is due to the rapidly increasing mortgage rates, which priced many home buyers out of homes that they could afford just a few months prior.

Image from Shutterstock

Image from Shutterstock

The Current Economy and Real Estate Market

As The Federal Reserve works to combat inflation by raising interest rates, companies are struggling to find enough employees to staff their operations, and the stock market is erasing value by billions of dollars, meaning our economy is going through a shaky period. Where we go from here is up to much debate, but time isn’t as much of an available option for military families as it is for civilians to wait for things to settle down again.

If a civilian purchased a home at the hypothetical top of the market and wants to sell as the home values are plummeting, they have the option of just sticking it out and waiting until prices recover (as they always do, eventually). In the military, however, that isn’t always up to us.

Because of our requirement to change duty stations so often, military homeowners may find themselves in a precarious situation if their home is suddenly underwater and it’s time to PCS. Your unit or commander isn’t likely to bend your departure date for a few years while you wait for the market to recover. This makes understanding the potential options far more important for servicemembers and their families than it is for civilians.

The Options

Living in Military Housing

Military housing differs greatly between duty stations, as do the regulations that determine who can or cannot live on base. This may not be your preferred option, but if money is tight or you're saving up for a home purchase in the future, it may be an excellent choice to save money. Some service members opt to take on mortgages that are budgeted based on their Basic Allowance for Housing (BAH) rates; however, all of your BAH will be used if you decide to live in military housing.

Renting off Base

Many civilians and service members alike look forward to the adventure of buying a new home or choose to see their home purchases as investments for the future. While home values typically increase over time, the requirements for constant moves in the military may not make a home purchase the best option for you. Especially when the economy is undergoing changes, renting may be the best option during shaky periods in the real estate market.

A year ago the cost to rent or own a home was virtually identical in many areas, but a recent report has outlined that it is now far more expensive to own a home rather than rent by as much as $839 per month. This differential is now higher than it has been at any point since the turn of the century.

Image from Canva

Image from Canva

Buy and Sell at PCS

A large number of service members and their families choose to purchase a home before or when they move to a new duty station, with plans to sell the home when they must move with their next orders. Typically this can work out very well for savvy home buyers, but as mentioned previously we are in a period of real estate where things are changing quickly.

Learn more: Should Military Rent or Own a Home? What to Know Before Deciding

Buy and Rent Out After PCS

Another option that some service members choose is to purchase a home when they get to their duty station, only to rent it out to others when their PCS orders come in. Whether this is planned in advance or becomes a preferred option because of changes in the real estate market, this can work out well if the proper research and planning are applied to the process.

As famed Rich Dad, Poor Dad author Robert Kiyosaki says when discussing real estate transactions, your primary residence (home) is not an asset for you— it’s an asset for your bank and a liability for you. This comment can cause vehement disagreements between some, but Kiyosaki’s thinking is that an asset should bring in revenue, not be purely a cost. Even if the plan is to sell the home for a profit in the future, at its current state as your primary residence it is a liability on your personal balance sheet.

If you do choose this option, it's extremely important that you consider the fact that you will not be living in the area after moving to your next duty station. New renters will have to be found every time old ones notify they plan to move out, repairs need to be kept up, HOA troubles may need to be handled, and any other number of issues taken care of that only homeowners know and understand.

The key to being able to do this successfully and headache-free is to find a trustworthy and hardworking yet affordable property manager who can do all of this for you. If you're in the military, it's highly likely that you know or work with someone who has direct experience working with property managers. Someone who was previously in your unit may have a local property manager that they have worked with and can suggest. Your unit’s spouse or family group may be an excellent resource for this, and many bases have working relationships with local REALTORS® and property managers.

This is not a person that should be chosen by a simple online search of property managers in your area. Do your due diligence to find someone who comes highly recommended. A property manager has to be trusted to manage and maintain a very expensive and valuable purchase that you're financially responsible for, while you are far away. Take the time to be sure that they can be trusted accordingly.

Image from Milstock Tribe

Image from Milstock Tribe

Military-Specific Risks to Home Buying

As mentioned previously, there are certain aspects of home buying and owning that affect service members in ways that civilians don’t have to worry about. If you're deciding whether or not to buy a new home, take care to consider these situations.

Security Clearance and Finances

If you're a member of or considering becoming a member of a unit or position that requires a security clearance, your finances need to be kept in extremely good working order. Many service members think they are cleared hot for any level of security clearance merely because they have never been arrested before, but security clearance investigations go much deeper than arrest records.

Especially if you are considering a move into intelligence, sensitive projects, or Special Operations, having your finances in good working order is a necessity to attain a security clearance. This doesn’t necessarily mean just staying out of debt, as living with expenses too close to your credit limit or owning more of a home or car than you can afford may also be red flags for sensitive mission or information-focused units.

Changes in the Housing Market Before the Next PCS

As we’ve mentioned several times, both our economy and the real estate market are in a bit of turbulence right now. Granted, real estate values typically increase over time, barring some type of unforeseen change in an area, such as Flint, Michigan, saw when the industry that many who lived there depended on (the automotive industry) moved out.

While civilians may have the luxury of waiting until a turbulent period passes, service members may not. If you're planning on purchasing a home, take care to do your research and have a backup plan should things change during the process or after your purchase. Homes are not something that you can just return for a refund, and 30 years is an awfully long time to have buyer’s remorse.

Home Upkeep While the Military Member Is Deployed

One aspect of home ownership that may not be considered in advance is the upkeep required to keep them in good shape. Since service members are constantly living under the potential of being deployed at a moment’s notice due to geopolitical events that they cannot see or control, this is something that should be greatly considered.

Whether you are a single service member or a married parent with children, take the time to consider who will care for the home’s upkeep should you be deployed. These can be small tasks that need to be constantly performed such as mowing and trimming the grass or large tasks such as replacing a water heater that goes out.

If you're a single service member who purchases a home and then is deployed during the winter months, who will check on your home for leaks or ensure the pipes don’t freeze? Those who live in condos or apartments have the luxury of building managers or HOAs who are responsible for the upkeep of the property, but once you own a home, that building manager is you.

As always, consider the potential issues in advance, and know who you can count on to take care of the property should you be suddenly called away for a school, field exercise, or deployment.

Image from Canva

Image from Canva

Closing

Buying your new home can be a rewarding, joyful, and amazing feeling that gives you intense satisfaction. Homeownership is part of the vaunted American dream, and who better to win at the American dream than those who serve her? If you’re willing to put your life on the line for those stars and bars, you deserve the world.

Despite our current turbulent economy, real estate values are one type of investment that has grown ad Infinitum as long as private land ownership has existed in society. Land was the very first asset of kings, and while gold is known to hold its value through bad times, real estate generally outpaces the performance of nearly any other asset aside from high-flying aggressive growth tech stocks (stocks that are not doing so hot right now, by the way).

When you've finally arrived at the point where you feel that you're financially prepared to begin looking for a new home, take the time to do your research. Cars and stocks are something that you can buy on a whim or because they catch your eye, but a home is a long-term contract and financial obligation.

As service members, we have things to consider that civilians don’t, and the typical real estate gurus or educational courses may not take those special considerations into mind when giving their advice. As long as you do your research, understand the environment that you are buying into, and have a contingency plan should anything change, owning your own home can be quite a satisfying and rewarding experience.

About the author: Robert is a former Army Special Forces medic and a multiple-tour veteran of OIF and OEF. He is the recipient of a Purple Heart, Bronze Star, and ARCOM among many other awards. Robert is an MBA who has bought properties in multiple states and has worked with many property managers and realtors, giving him first-hand experience in buying and selling real estate.

Thinking about buying a home? Grab our free resource below to help you make a decision.